Yo-Yo Financing: The Spot Delivery Scam That Traps Car Buyers (2026)

Table of Contents

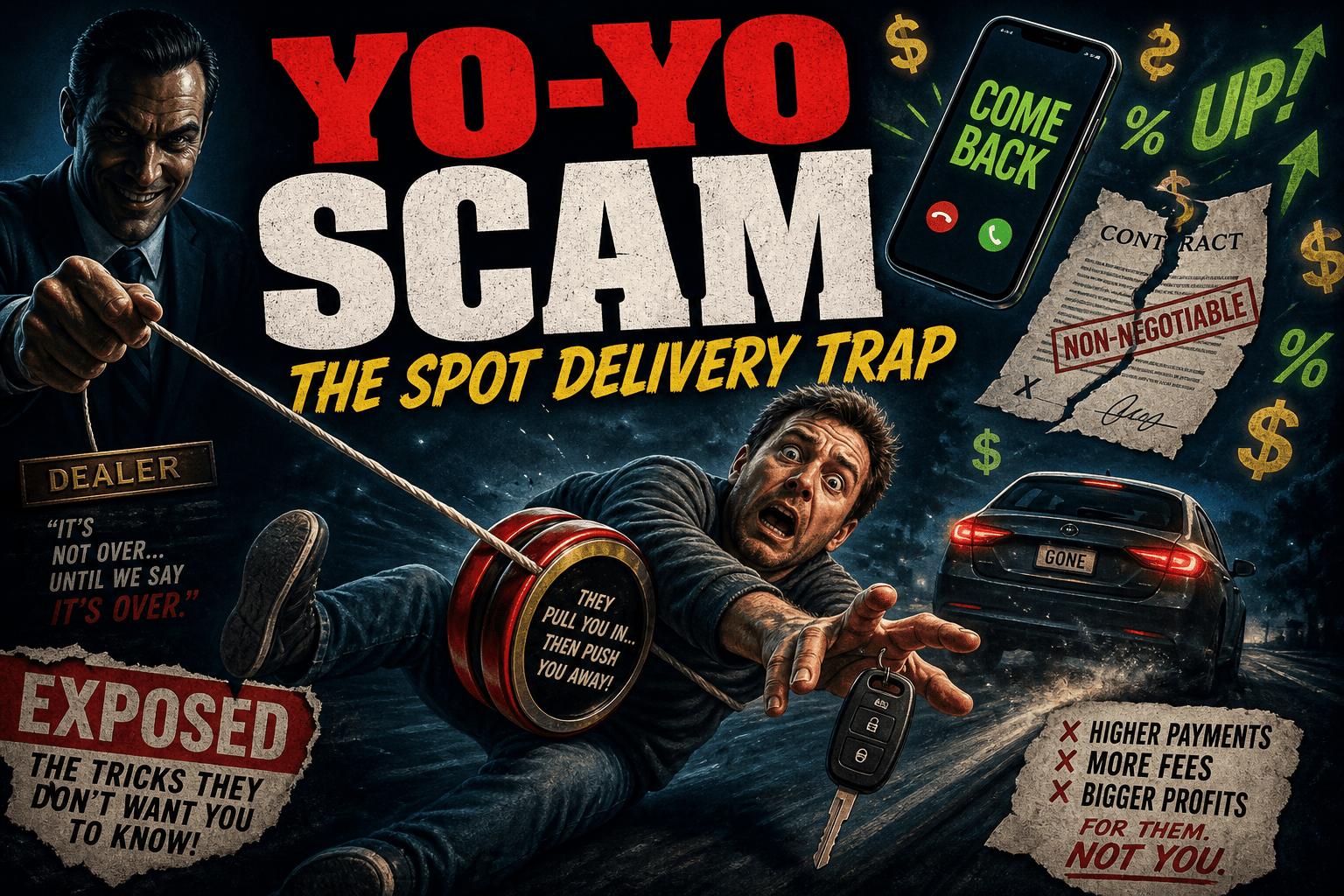

What Is Yo-Yo Financing?

Yo-yo financing (also called the "spot delivery scam") is one of the most predatory tactics in the car business. Here's how it works:

- You negotiate a deal, sign paperwork, and drive the car home

- Days or weeks later, the dealer calls: "Bad news — your financing didn't go through"

- They demand you come back and sign a new contract with a higher APR, bigger down payment, or both

- If you refuse, they threaten to repossess the car — even though you already signed a contract

The name "yo-yo" comes from the back-and-forth: the dealer sends you out with the car, then yanks you back on a string.

How Common Is This?

More common than you'd think. The FTC and state attorneys general receive thousands of complaints about spot delivery scams annually. It disproportionately targets:

- Buyers with lower credit scores (sub-650 FICO)

- First-time buyers with no credit history

- Young buyers who don't know their rights

- Military members stationed far from the dealership

The dealer knows these buyers are less likely to fight back or hire a lawyer.

The Anatomy of a Yo-Yo Deal

Here's what's really happening behind the scenes:

Step 1: The "Conditional" Contract

When you signed your paperwork, buried in the fine print was language like: "This contract is subject to financing approval." This is called a conditional delivery agreement or bailment agreement.

The dealer let you drive the car home before your loan was actually approved by a bank. Why? Because once you've:

- Told friends and family about your new car

- Posted on social media

- Started commuting in it

- Traded in or sold your old car

...you're emotionally and practically committed. Returning the car feels impossible.

Step 2: The "Bad News" Call

A few days to two weeks later, the finance manager calls with one of these scripts:

- "The bank needs a bigger down payment — can you bring in another $2,000?"

- "Your rate came back higher than expected — we need to adjust to 12.9% instead of 6.9%"

- "We need a co-signer, or we'll have to unwind the deal"

Step 3: The New (Worse) Deal

Now here's the critical question: did the financing actually fall through?

Sometimes, yes — the dealer genuinely couldn't place the loan. But often, this is a deliberate tactic:

- The dealer intentionally submitted your application to a lender they knew would reject it at the original terms

- They already had a backup approval at worse terms but showed you the good terms first to close the sale

- They're using the yo-yo to squeeze more profit from the deal

The result: you sign a new contract at $2,000–$5,000+ more over the life of the loan.

Your Legal Rights

This is where most buyers get it wrong. You have more power than the dealer wants you to believe.

Right #1: You Can Return the Car

If financing genuinely fell through and you haven't been approved, the original contract is void. You can return the car. But the dealer must also:

- Return your trade-in (in the same condition)

- Refund your down payment in full

- Cancel any add-on products you purchased

If they can't return your trade-in (because they already sold it), you have significant legal leverage.

Right #2: The Original Contract May Be Binding

In many states, if the dealer didn't include proper conditional delivery language in the contract, or if you weren't given a separate bailment agreement, the original contract may be fully binding — at the original terms. Consult your state's Attorney General or a consumer rights attorney.

Right #3: FTC Protections

The FTC's Combating Auto Retail Scams (CARS) Rule (effective 2025) specifically targets yo-yo scams. Dealers must:

- Disclose if delivery is conditional on financing

- Not misrepresent the terms of a deal

- Not charge for add-ons without consent

Violations can result in significant fines.

How to Protect Yourself

Before You Sign

- Get pre-approved through your own bank or credit union BEFORE visiting the dealer. If you already have financing, there's no "conditional" period.

- Read every document. Look for phrases like "subject to financing," "conditional delivery," or "bailment agreement." If you see them, ask: "Is my financing fully approved right now?"

- Ask directly: "Is this a spot delivery? Has the bank funded this loan?" Get the answer in writing.

If They Call You Back

- Don't panic. This is a negotiation, not a crisis.

- Don't sign anything new without taking time to review it.

- Ask for proof that the original financing was rejected — get the lender's denial letter.

- Know your options:

- Return the car and demand your full down payment + trade-in back

- Counter-offer: "I'll accept the new terms only if you reduce the vehicle price by $X to offset the rate increase"

- Contact your state's Attorney General consumer complaint line

- Consult a consumer rights attorney (many offer free consultations)

The Nuclear Option

If the dealer refuses to return your trade-in or down payment, or tries to report the car as "stolen":

- File a complaint with your state Attorney General

- File a complaint with the FTC at ftc.gov/complaint

- Contact a consumer attorney — yo-yo financing cases often result in settlements that exceed the value of the car

Red Flags of a Yo-Yo Setup

Watch for these warning signs at the dealership:

| Red Flag | What It Means |

|---|---|

| "Drive it home tonight!" pressure | They want you emotionally committed before financing is confirmed |

| Finance office rushing through paperwork | They don't want you reading the conditional delivery clause |

| Dealer asks you to leave your trade-in "for inspection" | They may sell it immediately to eliminate your fallback |

| Vague answers about loan approval | "We're still working on the best rate for you" = not approved yet |

| Weekend or holiday delivery | Banks are closed — financing literally can't be confirmed |

How DealerMath Decoder Helps

When you decode your deal with DealerMath Decoder, we flag any terms that look suspiciously different from your pre-approval. If the APR, payment, or loan term on the worksheet doesn't match what you were quoted, that's a red flag — and it's especially important to catch before you drive off the lot in a spot delivery scenario.

The Bottom Line

Yo-yo financing exploits your emotions and your lack of legal knowledge. The single best defense: get your own financing before visiting the dealer. If the dealer can't beat your rate, use yours. No spot delivery. No yo-yo. No stress.

- ✅ Get pre-approved from your bank or credit union first

- ✅ Ask if delivery is conditional on financing — get it in writing

- ✅ Never leave your trade-in until financing is confirmed

- ✅ Don't sign new terms without reviewing and counter-offering

- ✅ Use DealerMath Decoder to verify your numbers before driving off the lot