How to Negotiate a Car Price (2026 Step-by-Step Playbook)

Table of Contents

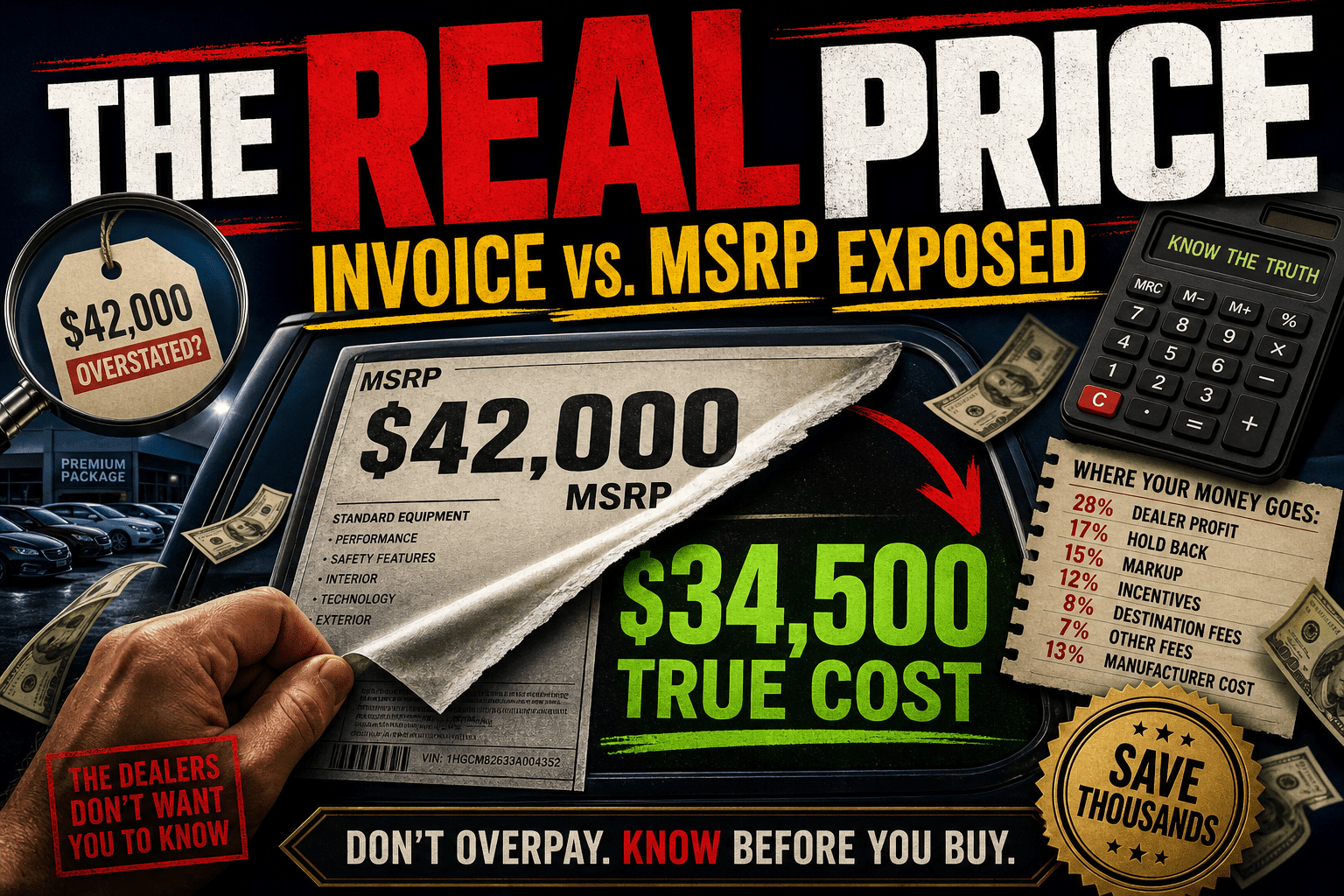

The Golden Rule: Negotiate the Total, Not the Payment

The single biggest mistake car buyers make is negotiating the monthly payment instead of the total price.

Here's why: a dealer can make any monthly payment look affordable by stretching the loan term. A $500/month payment on a 72-month loan costs you $36,000. That same payment on an 84-month loan costs $42,000 — that's $6,000 more for the exact same car.

Always negotiate the out-the-door (OTD) price — the total amount you'll pay including tax, fees, and everything else.

Before the Dealership: Your Prep Checklist

1. Know Your Numbers

- Research the fair market value on KBB, Edmunds, and TrueCar

- Check current incentives on the manufacturer's website

- Know your credit score — pull it free from annualcreditreport.com

- Get pre-approved financing from your bank or credit union (this is your leverage)

2. Get Competing Quotes

Email 3–5 dealerships within a 50-mile radius:

"I'm ready to purchase a [year/make/model/trim]. What is your best out-the-door price? I'm comparing offers from multiple dealers and will buy from whoever gives the best total price this week."

This forces dealers to compete on price before you even show up.

3. Set Your Walk-Away Number

Based on your research, set a firm maximum OTD price. Write it down. Do not exceed it no matter what the dealer says.

At the Dealership: The Negotiation Playbook

Step 1: Control the Conversation

When the salesperson asks "What monthly payment are you looking for?" — redirect:

"I'm focused on the total out-the-door price. What's your best number on this vehicle, all-in?"

Step 2: Let Them Go First

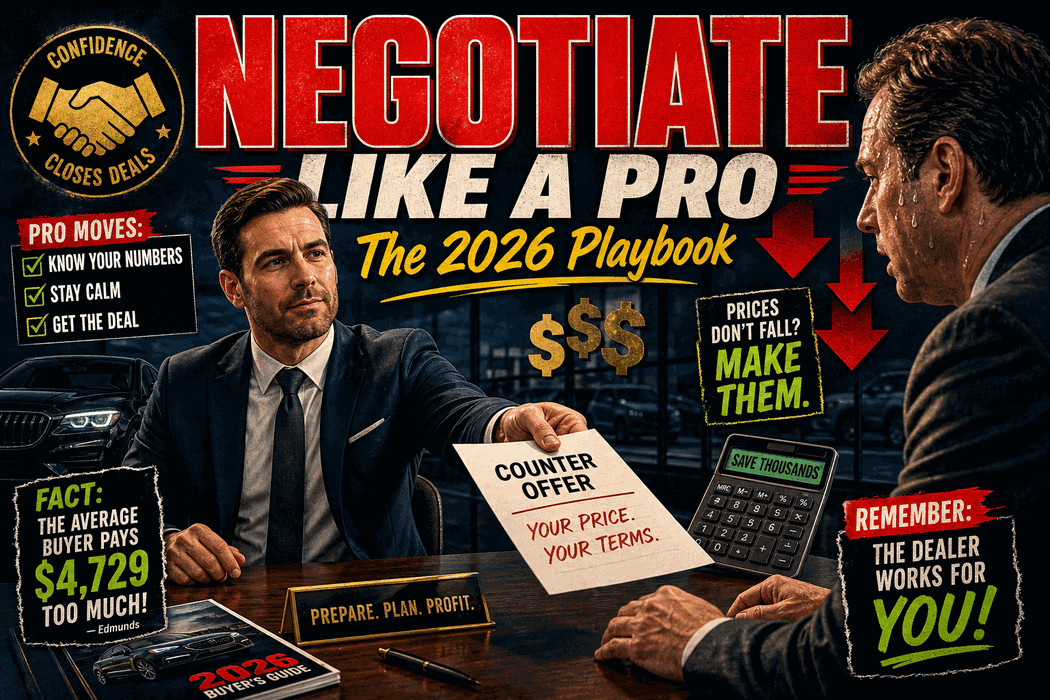

Never name your price first. Let the dealer make the opening offer. Their first number has profit margin built in — that's where the negotiation starts.

Step 3: Counter with Data

When they present their price, respond:

"I appreciate the offer. Based on my research, the fair market value for this vehicle is [your number from KBB/Edmunds]. I also have a quote from [competing dealer] at [$X]. Can you do better than that?"

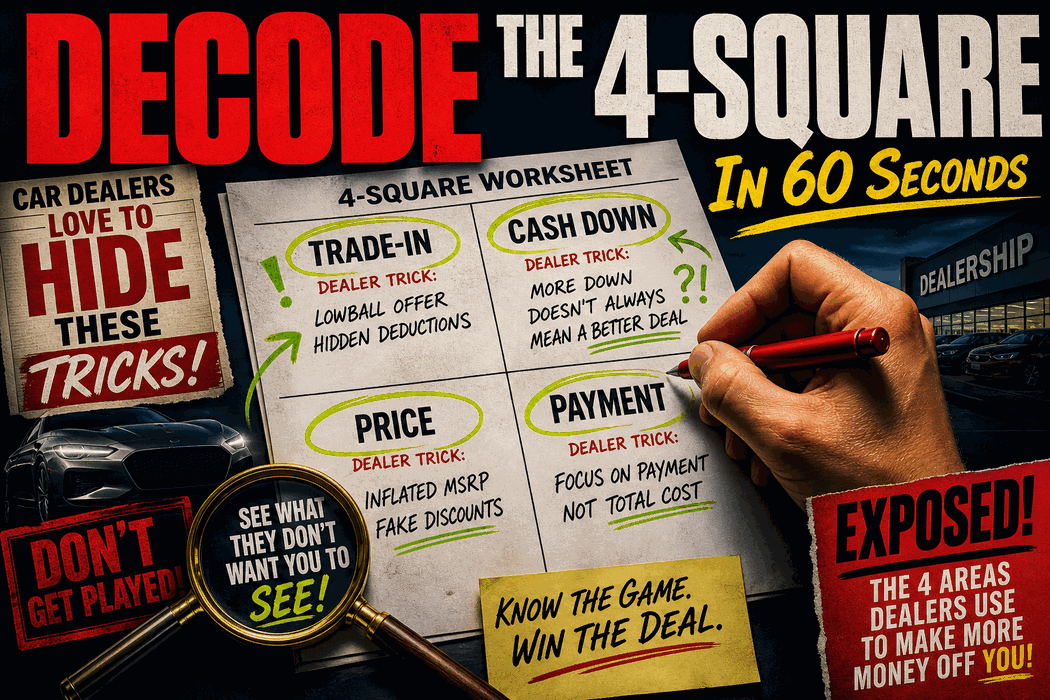

Step 4: Handle the "Four Square"

If the dealer pulls out a 4-square worksheet with four boxes (price, trade-in, down payment, monthly payment), they're trying to juggle numbers between the boxes to confuse you.

Your response:

"I'd like to keep this simple. Let's agree on the vehicle price first, then we'll talk about everything else separately."

Or better yet — take a photo of their 4-square and run it through DealerMath Decoder to see what they're really doing.

Step 5: Negotiate the Trade-In Separately

Only discuss your trade-in after you've locked in the purchase price. Get independent offers from CarMax, Carvana, or KBB Instant Cash Offer first — this gives you a floor.

"I have an offer of [$X] from CarMax. Can you match or beat that?"

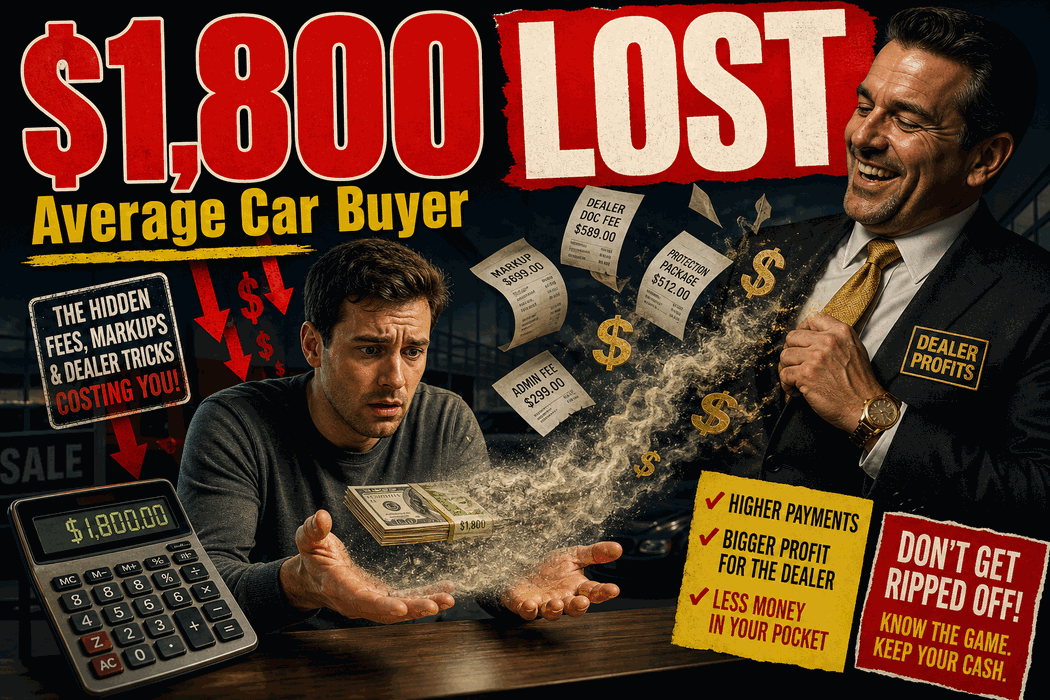

Step 6: The F&I Office

The finance manager will pitch:

- Extended warranty (usually 200–400% markup)

- GAP insurance (your credit union likely offers it for 1/3 the price)

- Paint protection, tire packages, etc.

It's okay to say no to everything. Just say:

"No thank you. I just want the vehicle as agreed."

Step 7: Review Before You Sign

Before signing ANYTHING, check:

- Vehicle price matches your negotiated number

- APR matches your pre-approval (or is better)

- Loan term is what you agreed to

- No add-ons or fees you didn't approve

- Trade-in value matches the agreement

Power Moves That Save Thousands

The "I'll Buy Today" Leverage

Dealers want to close deals today. Use it:

"If you can get the OTD price to [$your target], I'll sign right now. Otherwise I'll need to go with the other offer I have."

The Walk-Away

The most powerful negotiation tool: leave. Stand up, thank them for their time, and head for the door. In most cases, the manager will come out with a better number.

The End-of-Month Push

Dealers have monthly quotas. Shopping on the 28th–31st gives you maximum leverage. The discount they take to move one more unit can be substantial.

After the Deal: Verify Everything

Once you have the final numbers, run them through DealerMath Decoder to verify:

- You got a fair price vs. market value

- The APR matches your credit tier

- No hidden payment packing

- The doc fee and add-ons are reasonable

A 60-second decode can confirm you got a good deal — or reveal issues while you can still fix them.