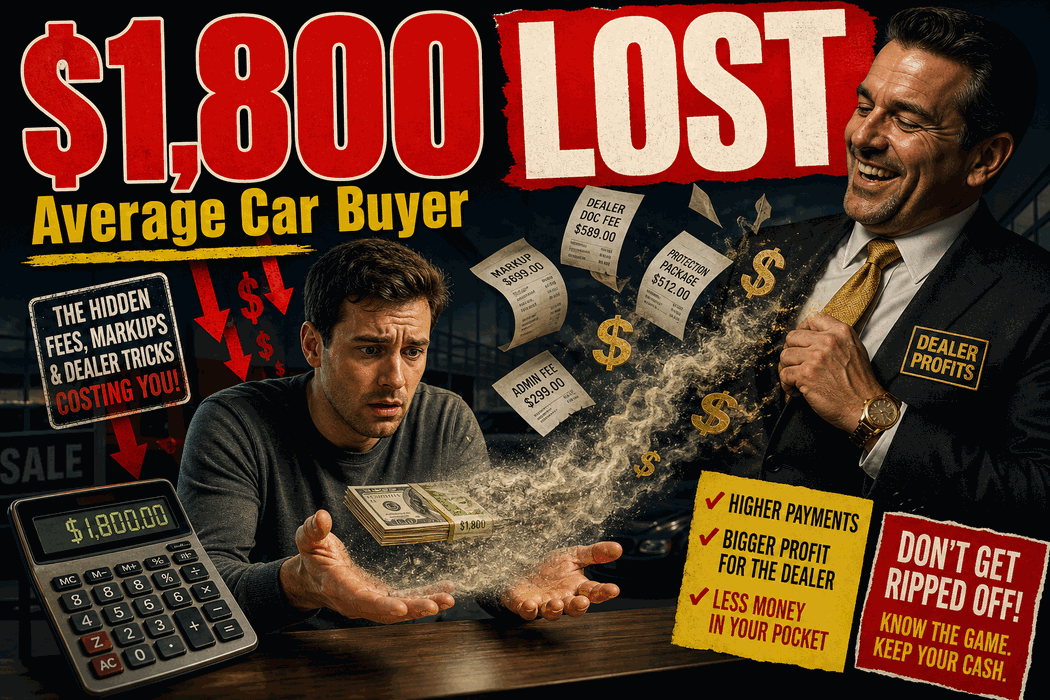

The Average Car Buyer Loses $1,800 — Here's Why (2026 Data)

Table of Contents

You probably think you got a "fair" deal on your last car.

Statistically — you didn't.

According to industry research from Cox Automotive, Edmunds, and NADA, the average new car buyer overpays by $1,800 on a single purchase. Used car buyers? $1,300. Lease buyers? Often more.

The shocking part isn't the number. It's that 92% of buyers never realize it happened.

This post breaks down exactly where that $1,800 goes, with real numbers from real dealer profit reports. By the end, you'll know the 7 hidden ways dealers extract profit — and how to stop each one in its tracks.

TL;DR — Where Your $1,800 Goes

If you're in a hurry, here's the breakdown of the average car buyer's losses:

- 💰 $487 — APR markup (the biggest profit center)

- 💰 $412 — Backend F&I products (extended warranties, GAP, etc.)

- 💰 $298 — Trade-in lowball

- 💰 $215 — Dealer-installed add-ons

- 💰 $187 — Inflated documentation fees

- 💰 $124 — Term stretching (longer loan = more interest)

- 💰 $77 — Misc. processing fees

- ━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

- 💸 $1,800 TOTAL in extracted profit

Now let's break down each one.

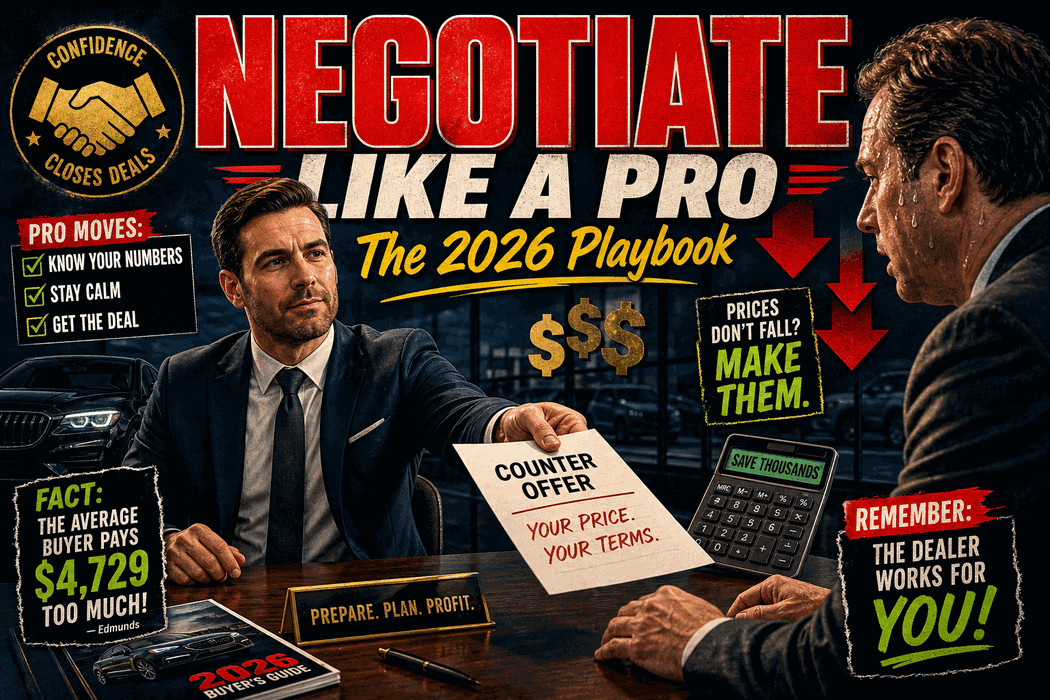

#1 — APR Markup ($487 average loss)

This is by FAR the biggest hidden profit center in modern car dealerships. It's also the most invisible to buyers.

How it works:

When the dealer "shops your loan" with banks, the bank approves you at a "buy rate" — say, 5.5% APR. The dealer is allowed to mark that up by up to 2.5% before presenting it to you. They give you the marked-up rate (8.0% APR), and they keep the difference as straight profit.

Real-world example:

$35,000 loan, 60 months At 5.5% APR (bank's buy rate): $668/mo, $5,099 total interest At 8.0% APR (marked-up rate): $710/mo, $7,571 total interest ───────── ───────────────── +$42/mo +$2,472 extra paid

The dealer gets a chunk of that $2,472 as commission. On average across all loans, this works out to $487 per deal.

How to stop it:

- Get pre-approved at your credit union BEFORE walking into the dealership

- Tell the F&I manager: "I'll accept dealer financing only if it BEATS my pre-approval rate"

- Ask to see the bank's actual buy-rate sheet (most won't show you — that's your answer)

#2 — Backend F&I Products ($412 average loss)

After you've negotiated the car price, you get sent to the "Finance & Insurance" office. This is where the REAL profit happens.

What they'll try to sell you:

• Extended warranty ($1,500-$3,500 markup) • GAP insurance ($500-$900 markup) • Tire & wheel protection ($400-$800 markup) • Paint/fabric protection ($600-$1,200 markup) • Service contracts ($1,000-$2,500 markup) • Key replacement coverage ($300-$600 markup) • VIN etching ($200-$400 — pure profit) • Nitrogen-filled tires ($150-$300 — useless)

The math you don't see:

The F&I office's markup on these products is often 100-300%. That extended warranty they're selling for $2,500? The dealer paid the warranty company $800 for it. The rest is profit.

How to stop it:

- Say this exact line: "I'm not buying any backend products today. Please skip directly to the contract."

- If they push back: "I've already declined every product. If you need to call your manager, that's fine — I'll wait."

- For GAP insurance — buy it from your own auto insurer for $30/year instead of $700 from the dealer

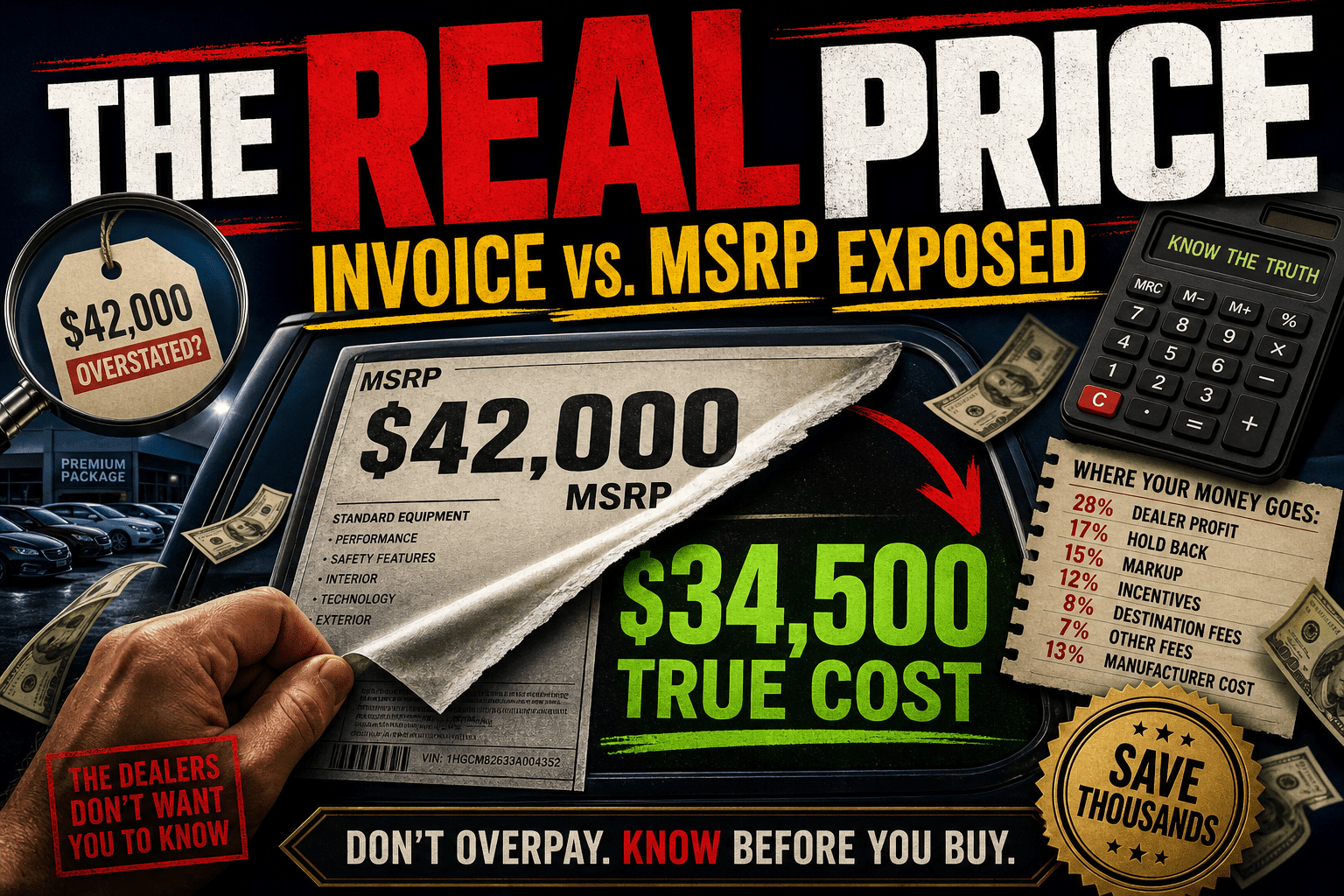

#3 — Trade-In Lowball ($298 average loss)

You drive your old car in. The dealer "appraises" it. They give you a number. You trust it because you're tired and want this over.

What's actually happening:

The dealer's appraisal team uses MMR (Manheim Market Report) wholesale auction data to determine what your car will fetch at auction. They then subtract their target profit margin (usually $1,500-$3,000) and offer you that number.

The buyer NEVER sees the MMR data.

Real-world example:

Your 2020 Honda Civic, average condition: MMR auction value: $13,500 Dealer's offer to you: $11,200 Their margin: $2,300

Carvana's online offer: $13,800 KBB Instant Cash Offer: $13,650 ───────── Lost by accepting dealer: $2,600

The "convenience" of trading in costs the average buyer $298 even AFTER they think they negotiated.

How to stop it:

- ALWAYS get an online offer from Carvana, CarMax, and Vroom BEFORE setting foot in a dealership

- Show the dealer the screenshots: "Match this or I sell to them after we close"

- Be willing to sell privately on Facebook Marketplace for an extra $1,000-$2,000

#4 — Dealer-Installed Add-Ons ($215 average loss)

This is the most blatant scam in modern car sales, and it's gotten worse since 2022.

What's happening:

When you arrive, the dealer presents a "build sheet" or "addendum sticker" showing:

• Window tint +$799 • Paint protection film +$1,499 • All-weather floor mats +$399 • Wheel locks +$299 • Pinstriping +$199 • "Theft deterrent" +$599 ────── TOTAL "REQUIRED" ADD-ONS: +$3,794

These are presented as non-negotiable because they're "already installed." The dealer's actual cost on these is usually 20-30% of what they're charging you.

The truth:

You can ALWAYS negotiate these off. Always. If a dealer refuses to remove dealer-installed add-ons, walk to the next dealer — they have the same cars.

How to stop it:

- "I want the car without any dealer add-ons. Please remove them from the sale price."

- If they refuse: "Then I'd like to see a vehicle without add-ons, or I'll find one at [competitor dealer]."

- Watch how fast they "find a way" to remove them

#5 — Inflated Documentation Fees ($187 average loss)

"Doc fees" cover the dealer's paperwork costs. The actual cost to a dealer for processing paperwork is around $40-$80.

What dealers charge:

States with doc fee caps: $75-$150 (regulated) States without caps: $399-$899 (predatory) Some Florida dealers: UP TO $1,295 😱

The truth:

Doc fees in unregulated states are NEGOTIABLE in many cases, even though dealers will swear they're not. The fee is set BY THE DEALERSHIP, not by the state.

How to stop it:

- Research your state's max doc fee online before walking in

- Ask: "What's your doc fee, and is it the lowest you can do?"

- If it's above $300: "I'll only sign if the doc fee is $200 or less. That's a profit center, not a real cost."

- If they hold firm: factor it into the final OTD price and reduce the vehicle price by the same amount

#6 — Term Stretching ($124 average loss)

You said you wanted a 60-month loan. Then somehow you walked out with an 84-month loan. How?

The sleight of hand:

The salesperson focuses your attention on monthly payment. They show you a worksheet with a 72-month or 84-month loan because the monthly payment LOOKS BETTER.

$35,000 loan at 7% APR:

48 months: $838/mo, $5,235 total interest 60 months: $693/mo, $6,584 total interest 72 months: $597/mo, $7,985 total interest (+$2,750 vs 48 mo) 84 months: $529/mo, $9,455 total interest (+$4,220 vs 48 mo)

You "saved $309/month" by stretching from 48 to 84 months — but paid an EXTRA $4,220 in interest.

The dealer profit: Many longer loans pay the dealer a higher reserve commission (more interest = more dealer cut).

How to stop it:

- Decide on your max term BEFORE walking in (60 months is the smart ceiling)

- "I want a 60-month maximum. Please show me payments at 60 months only."

- Never agree to extend the term to "lower the payment" — that's the trap

#7 — Misc. Processing Fees ($77 average loss)

This is the catch-all category: tiny fees buried in the contract that most buyers never question.

Common ones:

• "Electronic filing fee" $50-$150 • "Tag agency fee" $25-$75 • "Dealer prep fee" $100-$500 • "Lot management fee" $50-$200 • "Inventory transfer fee" $100-$300 • "Title processing fee" $25-$100

Many of these are completely fake fees invented to add small amounts of profit that buyers won't fight over.

How to stop it:

- Before signing, read EVERY line item on the contract

- Ask: "What is this fee for, exactly?"

- Many fees vanish when questioned — they're hoping you don't ask

The Real Total: Some Buyers Lose Way More Than $1,800

The $1,800 figure is the average. Some buyers lose far more.

According to Cox Automotive data:

- 12% of buyers lose more than $4,000

- 4% of buyers lose more than $7,500

- Lease buyers average $2,400 in hidden costs

- First-time buyers lose 34% more than experienced buyers

If you're young, female, a minority, or anxious — dealers statistically charge you more. This isn't opinion, it's documented in academic studies including the famous Northwestern University study showing female buyers were quoted prices $200-$500 higher than male buyers for the same car.

The math doesn't care who you are. But the salesperson reading you across the desk does.

How to Be in the 8% Who DON'T Overpay

The good news: it's not hard. Here's the system:

🛡️ The 5-Step Anti-Overpay System

Step 1: Lock in your financing FIRST

- Get pre-approved at a credit union (better rates than banks)

- Have the rate in writing on your phone

- This kills #1 (APR markup) and #6 (term stretching)

Step 2: Get 3 online trade-in offers BEFORE you go

- Carvana, CarMax, Vroom

- Use these as your floor — never accept less from a dealer

- This kills #3 (trade-in lowball)

Step 3: Get an OUT-THE-DOOR price by email before visiting

- Email 3-5 dealerships with the exact car you want

- Ask: "Please send me the out-the-door price, all fees included"

- The dealer with the cleanest OTD wins

- This kills #4 (add-ons), #5 (doc fees), and #7 (misc fees)

Step 4: Decline all F&I products

- Practice saying: "No backend products today, thank you"

- Repeat as needed

- This kills #2 (F&I markup)

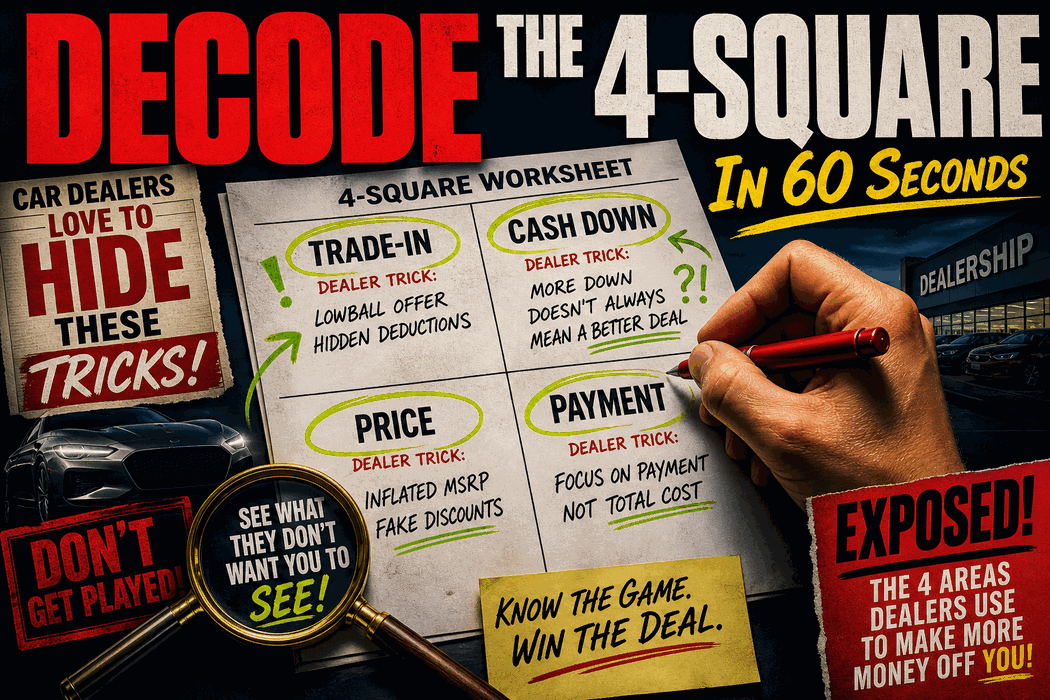

Step 5: Use a 4-square decoder at the desk

- Real-time math beats sales pressure every time

- Catches everything the previous steps missed

Run Your Deal Through the Decoder

If you're shopping right now — paste your numbers into DealerMath Decoder before you sign anything:

- ✅ See the true out-the-door price

- ✅ Detect APR markup vs. fair-market rates

- ✅ Spot inflated trade gaps

- ✅ Get a deal health score (0-100)

- ✅ Get scripts to push back on each red flag

Free. Works in 10 seconds. No signup required.

The Bottom Line

$1,800 is what the dealer industry makes off the AVERAGE buyer. That's not by accident — it's by design. Every box on the 4-square worksheet, every fee on the contract, every "let me check with my manager" pause is engineered to extract that $1,800.

The 8% of buyers who don't overpay have something in common: they refuse to negotiate on the dealer's terms. They come in pre-approved, pre-priced, and pre-researched. They walk in with information equal to (or greater than) the dealer's.

You can be in that 8%. The information is here. The tool is free. The next car you buy could be the first one where YOU win — not them.

Stop overpaying. Start decoding.