What Is a 4-Square Worksheet? Dealer Trick Explained (2026)

Table of Contents

The 4-square worksheet is the negotiation tool car dealers use to confuse buyers and hide profit inside your monthly payment. If you've ever sat across from a salesperson scribbling numbers into a four-box grid, you've seen one in action.

It looks innocent. It's just a piece of paper with four boxes: Price, Trade, Down, Payment. But that paper is engineered to confuse you, anchor you on the wrong number, and quietly extract an extra $2,000 to $5,000 out of your pocket before you sign.

This guide breaks down exactly what the 4-square is, what each box really means, the four most common tricks hidden inside it, and how to read one in under 60 seconds.

TL;DR

- The 4-square worksheet is a four-box grid dealers use during in-person negotiation

- The boxes are: Vehicle Price, Trade-In Value, Down Payment, Monthly Payment

- Dealers shift money between boxes to disguise hidden profit

- The real deal is out-the-door price + actual APR + loan term — not monthly payment

- The average buyer loses $2,000–$5,000 to 4-square tactics

- The free decoder tool below decodes any 4-square in 10 seconds

What Is a 4-Square Worksheet?

A 4-square worksheet (also called a "four-square," "deal sheet," or "T-sheet") is a single piece of paper divided into four equal quadrants. Car dealerships use it during the negotiation process to track and manipulate four key numbers in one place.

The four boxes are:

- 📍 Top Left — Vehicle Price: Sale price + dealer markup + add-ons

- 📍 Top Right — Trade-In Value: What they're "giving" you for your old car

- 📍 Bottom Left — Down Payment: Cash + manufacturer rebates you're putting down

- 📍 Bottom Right — Monthly Payment: The number they want you to focus on

The genius — and the danger — of the 4-square is that all four numbers are connected by math, but the math stays hidden. Change one box, and the others quietly shift in the dealer's favor.

When a salesperson says "let me run this by my manager," they're not actually negotiating with their boss. They're going in the back to recalculate which box to move money into so the deal looks better to you while staying just as profitable for them.

How the 4-Square Works (Real-World Example)

Let's walk through a real example. Say you're buying a $25,000 used Honda Civic with a $7,000 trade-in. You've told the salesperson you want to keep your monthly payment under $450.

Round 1: What the dealer writes

- Vehicle Price: $26,495

- Trade-In: $5,500

- Down Payment: $3,000

- Monthly Payment: $498/mo

You push back. "Too high. I want $400/month, and I want at least $7,500 for my trade."

The salesperson smiles, scribbles, walks to the back, returns.

Round 2: What the dealer writes

- Vehicle Price: $26,995

- Trade-In: $7,500

- Down Payment: $3,000

- Monthly Payment: $429/mo

You feel like you won. You got $2,000 more for your trade. The payment dropped by $69. You're about to sign.

What's actually happening behind the scenes:

- Trade-in shown: $7,500 → Real trade value: $7,500 (they had it all along)

- Vehicle price shown: $26,995 → They raised the price $500

- Verbal APR quoted: "6%" → Contract APR: 9.2%

- Term you assumed: 60 months → Actual term: 84 months

- Doc fee shown: Not mentioned → Actually charged: $1,495 (financed)

Result: You're paying ~$5,800 MORE over the life of the loan than you would have with honest math.

This is the 4-square trick in one sentence: the dealer gave you a "better" trade by quietly raising the price, stretching the term, and padding the APR — and you never noticed because you were watching the monthly payment.

Why Dealers Use the 4-Square Worksheet

The 4-square is taught in F&I training schools across the country for three specific reasons.

1. It anchors you to monthly payment

The bottom-right box is always the largest, boldest number. By design. Dealers know that buyers who focus on monthly payment will accept worse total costs in exchange for a $20/month reduction.

A $30 lower monthly payment over 72 months = $2,160 more in interest over the loan. But most buyers will sign because "$30 a month feels like nothing."

2. It mixes variables you can't track simultaneously

There are at least seven variables in any car deal: price, trade, down payment, APR, term, doc fee, and add-ons. The 4-square only shows you four of them. The other three (APR, term, fees) are quietly adjusted in the background.

By Round 3, you can't possibly remember what was in each box originally. You just want to be done.

3. It creates a sunk-cost effect

After two hours of back-and-forth, three rounds of trips to the manager, and a few "let me see what I can do for you" gestures, you feel invested in the deal. Walking away feels like wasting your whole afternoon.

That feeling is engineered. The 4-square ritual is designed to keep you in the chair until you sign.

The 4 Most Common 4-Square Scams

Once you understand the structure, the scams become obvious. Here are the four you'll see most often.

🚩 Scam #1: Trade-In Laundering

How it works: The dealer offers you MORE for your trade than it's worth — then quietly raises the vehicle price by the same amount.

Example:

- Your trade is worth $7,500 (per KBB)

- Dealer "generously" offers $9,000

- Vehicle price goes from $25,000 to $26,500

- You "win" on trade — but pay sales tax on the higher price and finance the same total amount

How to defend: Negotiate the vehicle price FIRST, in writing, with NO mention of your trade. Once that's locked, then negotiate the trade as a separate transaction. Better yet: sell your car privately on Carvana, CarMax, or Facebook Marketplace.

🚩 Scam #2: Term Stretching

How it works: You agreed to a 60-month loan. The contract shows 72 or 84 months. They never explicitly mentioned changing it — but the monthly payment "you wanted" only works with the longer term.

Example:

- $25,000 financed at 6% APR

- 60 months = $483/mo, $3,975 total interest

- 84 months = $365/mo, $5,652 total interest

- You "saved" $118/month but paid $1,677 more in interest

How to defend: Before signing ANYTHING, look at the Truth in Lending disclosure. It states the exact term in months. If it's longer than you agreed to — STOP and demand they fix it.

🚩 Scam #3: APR Markup (Dealer Reserve)

How it works: The bank approves you at 6%. The dealer tells you "the bank came back at 9%." The 3-point spread is pocketed by the dealer as "dealer reserve" — pure profit.

This is the single biggest hidden profit center in the modern car business. Dealers can mark up your APR by up to 2-3 points and pocket the difference, often $1,500-$3,000 per deal.

How to defend: Get pre-approved from your credit union BEFORE you walk into the dealership. Bring the approval letter. When they offer financing, ask them to beat your credit union's rate. If they can't (or won't show you the bank approval), use your credit union and ignore their offer.

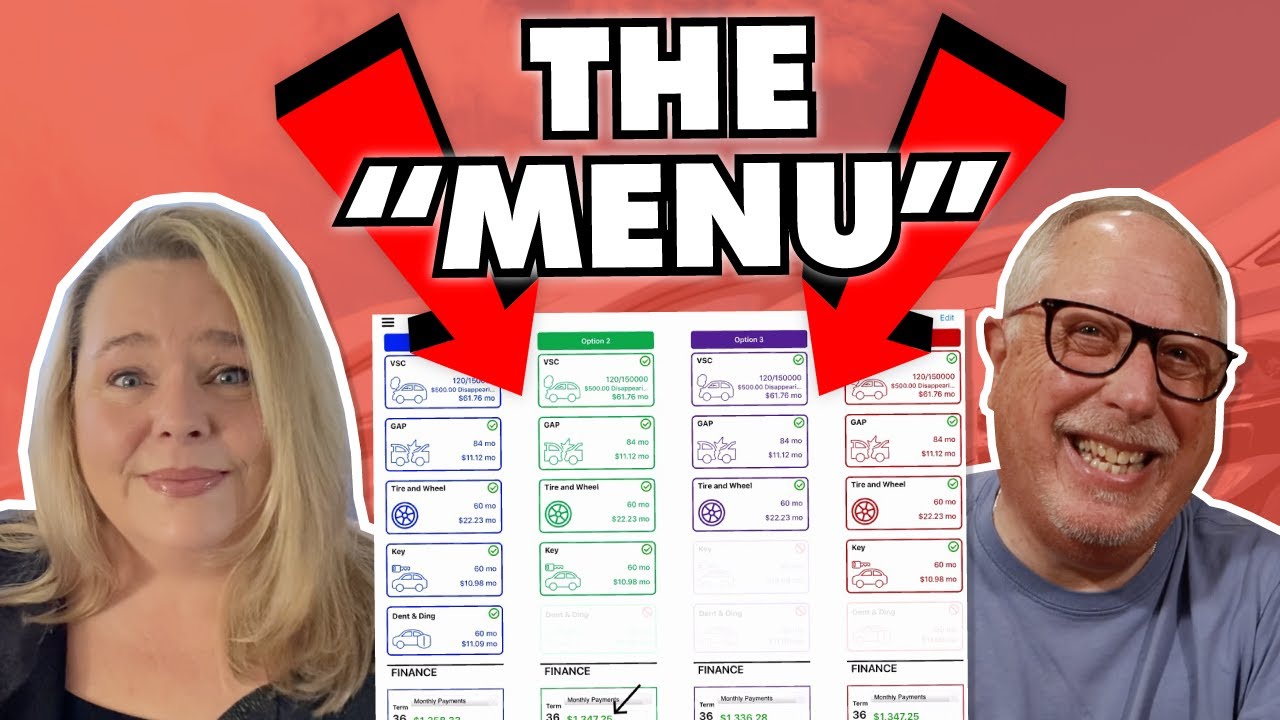

🚩 Scam #4: Payment Packing

How it works: In the F&I office (after the 4-square negotiation is "done"), the finance manager adds dozens of "small" products: GAP insurance, paint protection, tire & wheel coverage, key replacement, VIN etching, extended warranties.

Each one is presented as "only $15-$25 a month." Over 72 months, those small additions can total $4,000-$8,000 in pure dealer profit.

How to defend: In the F&I office, your default answer to every product offered is "No, thank you." GAP insurance and extended warranties can be bought from your credit union for 60-80% less. VIN etching, paint protection, and nitrogen-filled tires are pure profit with near-zero actual value.

How to Read a 4-Square Worksheet in 60 Seconds

When the salesperson slides the worksheet across the desk, do this in order:

- Find the vehicle price. Compare it to the advertised online price. Is it higher? By how much? Why?

- Find the trade-in number. Is it within $500 of your pre-researched KBB / Edmunds / Carvana offer?

- Find the down payment. Does it match what you said you'd put down?

- Find the monthly payment. Multiply payment × term. Add down payment + trade equity. Does the total make sense vs. the price?

- Ask: "What's the out-the-door price and the APR?" If they hesitate or won't write both numbers down in plain language — walk out.

If ANY of those five steps look wrong, stop. Don't sign. Don't keep negotiating. Just leave. There's always another dealer 15 minutes away with the same car or a comparable one.

What to Do BEFORE You Walk Into a Dealership

The 4-square only works if you walk in unprepared. Here's the pre-visit checklist that neutralizes 90% of dealer tactics:

- ✅ Get pre-approved at your credit union or bank — locks in your APR before negotiation starts

- ✅ Look up your trade-in value on KBB, Edmunds, and Carvana — get an actual offer from Carvana or CarMax as your floor

- ✅ Look up the market price for the exact car you want on Cargurus, Autotrader, and TrueCar

- ✅ Know your state's doc fee legal cap — many states cap it at $75-$200, but dealers still try to charge $500-$1,500

- ✅ Decide your maximum out-the-door price BEFORE you arrive — write it down and don't budge

- ✅ Tell the dealer up front: "I want to negotiate based on out-the-door price only. Please put it in writing."

Honest dealers respect this and will work with you. Dishonest dealers will resist — and that's your sign to walk out.

Decode YOUR 4-Square in 10 Seconds (Free)

We built DealerMath Decoder because too many car buyers were sitting at dealership desks signing 4-squares without understanding what they were really agreeing to.

Type in the four numbers from the dealer's worksheet → the tool instantly back-solves:

- ✅ True out-the-door price (including all hidden fees)

- ✅ Real APR vs. the verbal APR they quoted

- ✅ Trade-in markdown detection (are you getting your KBB value?)

- ✅ Term-stretch alerts (did they extend your loan without telling you?)

- ✅ Payment-pack alarm (are F&I add-ons hidden in your payment?)

- ✅ Red-Flag Scorecard (0-100 deal health score)

- ✅ Counter-scripts — the exact lines to say back to the salesperson

Free forever for the core tool. No signup required.

The Bottom Line

The 4-square worksheet is not a negotiation tool — it's a profit-hiding tool. Every box is connected by math the dealer controls and you can't see in real time.

But once you understand the four boxes, the four scams, and the five-step read, the 4-square loses its power. You walk into the dealership with the pre-visit checklist, you ask for out-the-door price in writing, and you decode any worksheet they hand you in under a minute.

Dealers count on confused buyers. Don't be one of them.